H. Roger Schwall, Assistant Director

U.S. Securities and Exchange Commission

Division of Corporation Finance

Mail Stop 4628

Washington, D.C. 20549-4628

|

Re:

|

Ur-Energy Inc. Form 20-F for the Fiscal Year Ended December 31, 2009

|

Dear Sir:

Ur-Energy Inc. ( “Corporation”) is in receipt of the comment letter from the staff (“Staff”) of the United States Securities and Exchange Commission (“SEC”) dated August 9, 2010 (“SEC Letter”) regarding the Corporation’s Annual Report on Form 20-F for the fiscal year ended December 31, 2009 (“2009 Form 20-F”) filed with the SEC on March 12, 2010. The Corporation’s responses to the comments are set forth below. For convenience, the comments in the SEC Letter are reproduced below.

Engineering Comments

General

|

1.

|

Comment 1. We note that your website refers to or uses the terms “measured,” “indicated,” and “inferred,” resources. If you continue to make references on your web site or press releases to reserve measures other than those recognized by the SEC, please accompany such disclosure with cautionary language comparable to the following:

|

Cautionary Note to U.S. Investors – The United States Securities and Exchange Commission permits U.S. mining companies, in their filings with the SEC, to disclose only those mineral deposits that a company can economically and legally extract or produce. We use certain terms on this website (or press release), such as “measured,” “indicated,” and “inferred” “resources,” which the SEC guidelines strictly prohibit U.S. registered companies from including in their filings with the SEC. U.S. Investors are urged to consider closely the disclosure in our Form 20-F which may be secured from us, or from our website at http://www.sec.gov.edgar.shtml.

Please indicate the location of this disclaimer in your response.

H. Roger Schwall

Assistant Director, SEC

August 20, 2010

Page 2

Response to Comment 1. As requested in the SEC Letter, a Cautionary Note to U.S. Investors has been added to the Corporation’s website (www.ur-energy.com), as follows:

Cautionary Note to U.S. Investors: The terms “mineral resource,” “measured mineral resource,” “indicated mineral resource” and “inferred mineral resource,” as used on our website are Canadian mining terms that are defined in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”). These Canadian terms are not defined terms under United States Securities and Exchange Commission (“SEC”) Industry Guide 7 and are normally not permitted to be used in reports and registration statements filed with the SEC by U.S. registered companies. The SEC permits U.S. companies, in their filings with the SEC, to disclose only those mineral deposits that a company can economically and legally extract or produce. Accordingly, note that information contained on this website describing the Company’s “mineral resources” is not directly comparable to information made public by U.S. companies subject to reporting requirements under U.S. securities laws. U.S. investors are urged to consider closely the disclosure in our Form 20-F which may be secured from us, or online at http://www.sec.gov/edgar.shtml.

This Cautionary Note to U.S. Investors has been included on the following pages on the Corporation’s website: www.ur-energy.com/about-ur-energy/; www.ur-energy.com/lost-creek/; www.ur-energy.com/other-wyoming-projects/; and www.ur-energy.com/technical-reports/.

Information on the Corporation page 10

|

2.

|

Comment 2. We note the references to your company as a “development” stage company throughout your disclosure. As the company does not have a “reserve,” it must be in the “exploration stage,” as defined by Industry Guide 7(a) (1) and (a) (4) (i) respectively. Please modify your disclosure accordingly, removing all references to “development” or “development stage.”

|

Response to Comment 2. Pursuant to Canadian generally accepted accounting principles (“Canadian GAAP”), the Corporation has reported its financials and other disclosures as a “development stage” company, including in its 2009 Form 20-F, which is a dual-purpose document also used as an Annual Information Form that is filed with the securities regulatory authorities in Canada. Canadian GAAP considers a company which is devoting most of its efforts to developing natural resources to be a development stage enterprise (see AcG-11 Accounting Standards for “enterprises in the development stage” (“AcG-11”), para. 2). Pursuant to AcG-11, the fact that the enterprise is in the development stage should be disclosed, including the nature of development activities and the planned principal operations of the enterprise (see AcG-11, para. 29 and para. 31).1

1 Generally accepted accounting principles in the United States (“US GAAP”) require similar accounting treatment of development stage companies. Section 915-10-05-1 in the U.S. Accounting Codification (formerly FASB 7), defines a development stage entity as one which, among other things “is devoting most of its time to raising capital, exploring for natural resources and developing natural resources.”

H. Roger Schwall

Assistant Director, SEC

August 20, 2010

Page 3

In accordance with Canadian GAAP, the Corporation is described as “a development stage junior mining company engaged in the identification, acquisition, evaluation, exploration and development of uranium mineral properties in Canada and the United States.” Item 4.A at page 14. The Corporation is engaged in the identification, acquisition, evaluation and exploration of various uranium mineral properties, and is currently advancing its Lost Creek project in Wyoming to become a uranium in situ recovery mine as more fully described in the Company’s 2009 Form 20-F. The development of the Lost Creek deposit toward mine production has included more than 500,000 feet of drilling in the past two years, in order to design and delineate the first two mine units for production. The design of the production facility is complete and a general contractor selected; long lead-time equipment has been designed, ordered and partially fabricated. All other equipment and facilities have been designed and bid for purchase or development. The initial applications for permitting and licensure of the project were submitted nearly three years ago, and have since been progressing through the regulatory processes with federal, state and local authorities.

As described above, the Corporation generally meets the SEC standards of a development stage company set forth in Industry Guide 7(a)(4)(ii) which defines “Development Stage” to include “all issuers engaged in the preparation of an established commercially minable deposit (reserves) for its extraction which are not in the production stage.” The Corporation meets this definition, except for “reserves,” as it is currently preparing its Lost Creek deposit for mineral extraction. The development of uranium in situ recovery projects is unique in mineral extraction, and is not specifically contemplated within the Canadian Institute of Mining, Metallurgy and Petroleum (“CIM”), or U.S. regulatory, definitions for the ready estimation of a “mineral reserve.” This is summarized in the 2009 Form 20-F in Item 5 at page 30. As stated in the National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) 2008 Lyntek Preliminary Assessment for the Lost Creek Project (“Lyntek Report”): “Since the practice of ISR mining is to drill out individual mine units just prior to mining each unit, this Preliminary Assessment report can only use indicated mineral resources which are considered too speculative geologically to have economic considerations applied to them to be categorized as Mineral Reserves.” Item 4.B at page 19. This circumstance is also relevant to the Corporation’s Response to Comment 5, below.

As a result of the mining method and development of the mine (mine unit by mine unit just prior to mining; the Lyntek Report anticipates six mine units), there is no economically reasonable means of determining a mineral reserve of the entire deposit prior to mining. If the reference to “development stage” is limited to mining companies that only have reserves, an in situ recovery mining company advancing its first project would, therefore, be an exploration stage company one day and a production stage company the next, never permitted to refer to itself as a development stage company. The Corporation believes that the absence of the reference to “development stage” in its disclosure could cause confusion for investors.

Because of the application of Canadian GAAP, and the status of the Lost Creek in situ recovery uranium project, the Corporation has used the terminology “development stage” to satisfy accounting principles and to properly explain that the Corporation is at a development stage

H. Roger Schwall

Assistant Director, SEC

August 20, 2010

Page 4

rather than an exploration stage, which would have different risks, different speculative value, and a different timeline to the expectations upon becoming a production stage company.

|

3.

|

Comment 3. We note your disclosure of a non-National Instrument 43-101 compliant resource throughout your filing. With the passage of National Instrument 43-101 in Canada, disclosure using non-SEC reserve definitions and resource estimates is allowed for Canadian incorporated companies under the exception in Instruction 3 to Paragraph (b)(5) of Industry Guide 7. However, all mineral reserve or resource estimates that you disclose under this provision must meet the standards of National Instrument 43-101. Since you disclose that you cannot confirm that such information is in compliance with NI 43-101, you may need to remove disclosure of the related estimates.

|

Response to Comment 3. The Corporation believes that the description of new exploration targets on and adjacent to the Lost Creek permit area meets the requirements of NI 43-101.

The disclosure of ranges of quantity and grade, as set forth with certain qualifications, is specifically permitted pursuant to NI 43-101, Section 2.3(2). Section 2.3(2) provides that “an issuer may disclose in writing the potential quantity and grade, expressed as ranges, of a potential mineral deposit that is to be the target of future exploration if the disclosure (a) includes a statement that the potential quantity and grade is conceptual in nature, that there has been insufficient exploration to define a mineral resource and that it is uncertain if further exploration will result in the target being delineated as a mineral resource; and (b) states the basis on which the disclosed potential quantity and grade has been determined.”

The Corporation believes that the disclosure regarding these new exploration targets sets forth ranges of quantity and grade of uranium, and resulting estimates regarding a potential deposit, while specifying that it is not describing a compliant resource estimate. Item 4.A at page 15; Item 5 at page 35. The disclosure continues by explaining that the ranges and identification of the new exploration targets are based upon historic drill results and a lengthy, in-depth geologic evaluation performed in 2009 by Corporation geologists in which similarities were identified between the alteration characteristics and grade thickness of the drill data to Lost Creek data. Item 4.A at page 15; Item 5 at page 35. The disclosure further states that the estimate and evaluation are only conceptual in nature, and that there is insufficient exploration to yet define a mineral resource, concluding that it is uncertain whether further exploration will result in delineation of a mineral resource. Item 4.A at page 15; Item 5 at page 35.

Business Overview page 12

|

4.

|

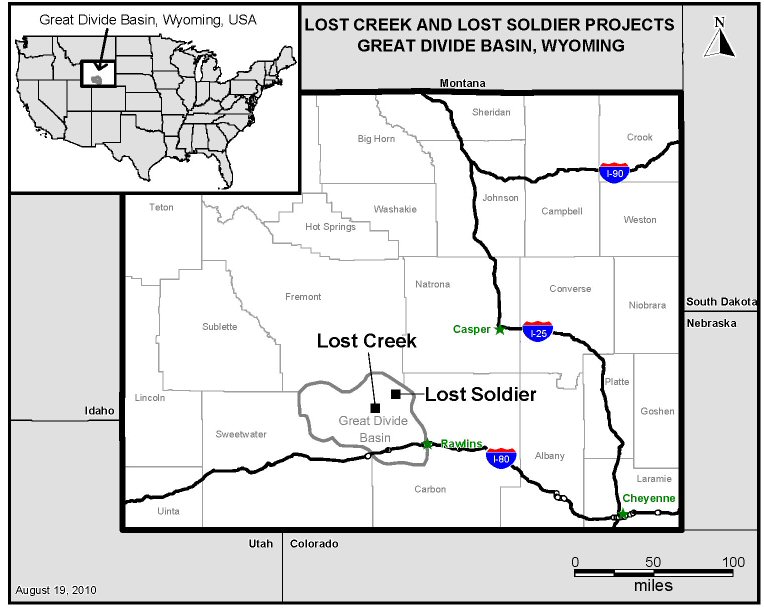

Comment 4. Please insert a small-scale map showing the location and access to each material property, as required by Instruction 1(a) to Item 4.D of Form 20-F. We believe the guidance in Instruction 1(a) to Item 4.D of Form 20-F would generally require maps and drawings to comply with the following features: (1) A legend or explanation showing, by means of pattern or symbol, every pattern or symbol used on the map or drawing; (2) A graphical bar scale should be included; (3) Additional representations of scale such as “one

|

H. Roger Schwall

Assistant Director, SEC

August 20, 2010

Page 5

inch equals one mile” may be utilized provided the original scale of the map has not been altered; (4) A north arrow; (5) An index map showing where the property is situated in relationship to the state or province, etc., in which it was located; and (6) A title of the map or drawing, and the date on which it was drawn. In the event interpretive data is submitted in conjunction with any map, the identity of the geologist or engineer that prepared such data. Any drawing should be simple enough or of sufficiently large scale to clearly show all features on the drawing.

Response to Comment 4. The Corporation intends to include, as an amendment to Item 4.B of the 2009 Form 20-F, a map showing the location of the Lost Creek and Lost Soldier projects in the form provided as Schedule A hereto. Item 4.D (specified in Comment 4) provides a cross reference to Item 4.B for a detailed description and background of each of the Corporation’s material properties, specifically Lost Creek and Lost Soldier.

The Corporation believes that descriptive features requested in reference to the map, such as the geologic reference to the location of the Lost Creek and Lost Soldier deposits (the Great Divide Basin, Wyoming) and detailed descriptions of the geographical locations are consistently made in the Corporation’s narrative disclosures. See Item 4.A at page 14; Item 4.B at pages16, 21, 22 and 23; Item 5 at pages 30, 32, 33 and 35.

|

5.

|

Comment 5. We note your disclosure of economic indicators in this section and throughout your filing that are based on resources and preliminary economic assessments. These estimates do not have a demonstrated economic viability as may be implied. Therefore, please remove the financial information developed and/or derived from the possible development of your resources. This would include your operating cash flow, operating costs, capital expenditures, net present value, and payback period. Please modify your filing accordingly.

|

Response to Comment 5. As discussed in Response to Comment 2, above, and summarized in Item 5 at page 30 of the 2009 Form 20-F, the mining method to be used at Lost Creek, in situ recovery, and the CIM definitions of reserves do not permit the financially reasonable, ready estimation of mineral reserves. Notwithstanding the impracticality of most in situ uranium projects to determine a reportable mineral reserve, it is correctly noted in Comment 6 below, that even an NI 43-101 compliant mineral resource has reasonable prospects of being economically extracted.

The CIM definition of Mineral Resource is “a concentration [of mineral] in such form and quantity and of such a grade or quality that it has reasonable prospects for economic extraction.” The CIM definition of Indicated Mineral Resource is “that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics can be estimated with a level of confidence sufficient to allow the appropriate application of technical and economic parameters, to support mine planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and

H. Roger Schwall

Assistant Director, SEC

August 20, 2010

Page 6

drill holes that are spaced closely enough for geological and grade continuity to be reasonably assumed.”

The Lyntek Report employed a conservative approach in its preliminary assessment, using an indicated resource number of 8.1 million pounds in its conceptual model of six mine units, with an 80% recovery resulting in estimated production of approximately 6.5 million pounds. It is upon the confidence supplied by the underlying geologic resource estimate, the Lyntek Report modeling and subsequent further evaluation that mine planning and development has proceeded over the past several years. See Item 4.B at 19 and 21; see also Response to Comment 2, above. It is notable that the CIM definitions comment that an “Indicated Mineral Resource estimate is of sufficient quality to support a Preliminary Feasibility Study, as defined in NI 43-101, which can serve as the basis for major development decisions.” The Lyntek Report provides eight separate economic cases, substantiated by geologic, engineering and financial data, detailed analysis, and reasonable assumptions. The mineral resource estimate for Lost Creek has never been represented to be a mineral reserve. The Lyntek Report was titled a “Preliminary Assessment” in compliance with NI 43-101 because, in the absence of mineral reserve estimates, the Lyntek Report cannot satisfy the complete definitions of the “pre-feasibility” and “feasibility” under NI 43-101, Section 1.1. See also NI 43-101, Section 2.3(4).

Again, the Corporation’s disclosure was made in an effort to most completely describe the status and development of the Lost Creek in situ recovery project to mine production. See Instructions to Form 20-F General Instructions C (c)(citing Exchange Act Rule 12b-20); see also National Instrument Form 51-102 F2 General Instructions and Interpretation Part 1 (d) and (e).

|

6.

|

Comment 6. All mineral resources have the requirement of reasonable prospects for economic extraction. This requires the use of preliminary economic, mining, metallurgical, environmental, and pricing information to constrain your mineral envelope. Please ensure this basic information is disclosed for each of the resource estimates in your filing. This basic information should include tons, grade, cut-off grade, assumed metal price, mining recovery, and metallurgical recovery. For simplicity, we suggest the tonnage and grade for your reserves and/or resources are listed in a table with the economic criteria listed as footnotes.

|

Response to Comment 6. The Corporation believes that the information requested in Comment 6 is already included in the 2009 Form 20-F. The Corporation recognizes that not all of the information requested is reflected in chart or table form. This is in large part due to the fact that the data appears in excerpts from three NI 43-101 Technical Reports related to the Lost Creek and Lost Soldier projects, the text of which was not altered for insertion in the 2009 Form 20-F, as these NI 43-101 Technical Reports are documents that have been previously filed with Canadian securities regulators and the SEC. The Corporation believes that all required information does appear in the text and tables excerpted from those NI 43-101 Technical Reports: in respect of Lost Creek, the disclosure appears at Item 4.B at pages 18 and 21 (tons, grade); Item 4.B at pages 18 and 22 (cut off grade); Item 4.B at pages 20 and 22 (assumed metal price); Item 4.B at pages 19, 21 and 22 (mining and metallurgical recovery); and in respect of Lost Soldier, the disclosure appears at Item 4.B at page 23 (tons, grade and cut off

H. Roger Schwall

Assistant Director, SEC

August 20, 2010

Page 7

grade); Item 4.B at page 25 (assumed metal price); Item 4.B at pages 23 and 24 (mining and metallurgical recovery). It may be noted, as well, that all data sought in Comment 6, except for metal price, is initially presented in summary form at the beginning of each of the NI 43-101 Technical Reports, other than the Lyntek Report, related to Lost Creek and Lost Soldier. Item 4.B at pages 21 and 23. Due to the sometimes duplicative nature of the information contained in this dual-purpose filing as both an Annual Information Form and Form 20-F, the Corporation was, and remains, concerned that the insertion of additional, largely duplicative charts or tables would potentially cause confusion in the disclosure.

In connection with this response to the SEC Letter, the Corporation acknowledges that it is responsible for the adequacy and accuracy of the disclosure in the filing; and further acknowledges that Staff comments or changes to disclosure in response to Staff comments do not foreclose the SEC from taking any action with respect to the filing; and, further acknowledges that the Corporation may not assert Staff comments as a defense in any proceeding initiated by the SEC or any person under the federal securities laws of the United States.

Sincerely,

Ur-Energy Inc.

| By: |

|

/s/ Roger L. Smith |

| |

|

Roger L. Smith

Chief Financial Officer

|

| |

|

|

| |

|

|

| Encl. |

|

|

| |

|

|

| c: |

|

Thomas Rose, Troutman Sanders LLP

Virginia Schweitzer, Fasken Martineau DuMoulin LLP

|